Originally published: November 6, 2015 | Last updated: December 18, 2024

TL;DR: Blended families face unique estate planning challenges. Without Wills, stepchildren inherit nothing, surviving spouses may not receive the family home, and children from prior relationships can be inadvertently disinherited. Key strategies include life interest provisions, carefully chosen executors, trusts for minors, and a complete estate plan with Powers of Attorney and Living Wills.

Blended families which include children from previous relationships between partners have become a common family structure across Canada. The process of estate planning for blended families presents more challenges than traditional nuclear families because stepchildren and biological children and current and former spouses maintain different claims to the estate. The forced distribution of blended family assets through intestate succession laws leads to terrible outcomes when people fail to create proper succession plans. Blended families require a properly developed Will as their fundamental requirement for their future security.

Blended families, where one or both partners have children from previous relationships, are increasingly common in Canada. Estate planning for blended families is significantly more complex than for traditional nuclear families because the interests of stepchildren, biological children, and current and former spouses can conflict. Without careful planning, intestate succession laws produce results that are often devastating for blended families. A well-crafted Will is not optional for blended families, it is essential.

What Happens If a Blended Family Has No Wills?

Consider a common scenario: Dan and Sue are married. Dan has two children from a previous marriage, and Sue has one child from hers. If Dan dies without a Will, provincial intestate succession laws determine how his estate is split; typically between Sue and Dan’s biological children. Sue’s child receives nothing from Dan’s estate. If the family home is in Dan’s name, Sue may be forced to sell it to pay Dan’s children their share. None of this reflects what Dan likely would have wanted.

The complications multiply if Sue then dies without a Will. Her estate goes to her biological child only. Dan’s children from his first marriage receive nothing from her, even if they lived together as a family for decades. The combined effect is that stepchildren are completely excluded from both estates, while biological children may receive disproportionate shares depending on which parent dies first.

Dan and Sue live together as husband and wife in a typical family setup. Dan brings two children from his previous marriage while Sue brings one child from her previous marriage. The provincial intestate succession laws determine how Dan’s estate will be divided when he passes away without creating a Will. The child of Sue receives no money from Dan’s estate. The family home which belongs to Dan requires Sue to sell the property because she needs to pay Dan’s children for their ownership rights. The situation shows no evidence about what Dan would have selected.

Sue’s death without a Will creates new challenges which need to be resolved. Her estate goes to her biological child only. Dan’s children from his first marriage receive nothing from her, even if they lived together as a family for decades. The two effects merge to remove stepchildren completely from both estates while biological children receive uneven inheritance amounts depending on which parent passes away first.

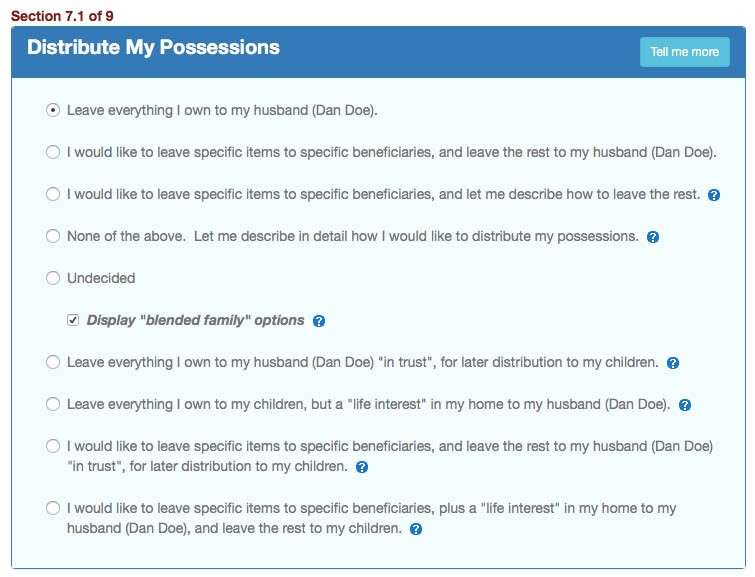

A life interest (also called a life estate) allows your surviving spouse to use and benefit from your assets during their lifetime, with the assets passing to your children after the spouse dies. For example, Dan could grant Sue the right to live in the family home for the rest of her life, with the home passing to Dan’s children upon Sue’s death. This protects both the surviving spouse’s housing security and the children’s eventual inheritance. It is one of the most effective tools for balancing competing interests in a blended family.

What Estate Planning Strategies Work for Blended Families?

Executor selection is critical in blended families. Naming your current spouse as executor can create a conflict of interest if they are also a beneficiary whose interests may compete with your children’s. Options include naming an independent third party, a professional executor, or co-executors (one from each “side” of the family). The executor must be someone who will carry out your wishes faithfully, even when those wishes require balancing the needs of a surviving spouse against the interests of children from a prior relationship.

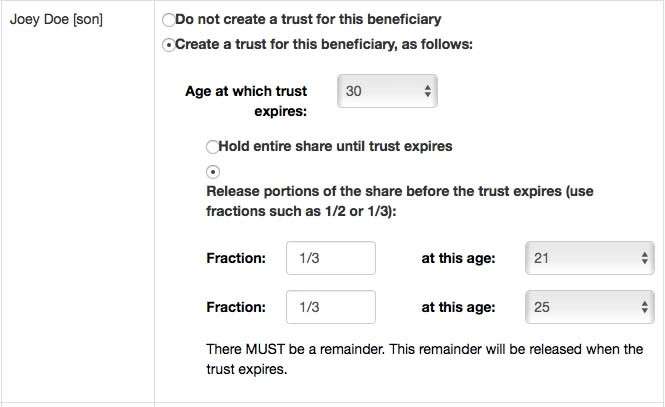

Consider this scenario: Dan leaves $100,000 to his 16-year-old son outright, without a trust. Two years later, the son turns 18 and has full access to the money. He buys a sports car and spends the rest within a year. With a trust, the money would have been managed by a responsible adult trustee, available for education and necessities, with the remainder released at a more mature age like 21 or 25. The trust protects both the money and the child from poor financial decisions made at a young age.

Life Interest in the Estate

Yes. Unlike intestate succession laws (which exclude stepchildren entirely), a Will allows you to include anyone you choose as a beneficiary, including stepchildren, step-grandchildren, or any other person. You can leave them specific gifts, percentages of your estate, or name them as residual beneficiaries. For blended families, explicitly naming stepchildren is often one of the most important reasons to write a Will. Without being named in a Will, a stepchild has no legal claim to a step-parent’s estate in any Canadian province, regardless of how close the relationship was or how long they lived together as a family.

Your surviving spouse will receive a life estate from your assets which allows them to use these assets until their death at which point your children will receive the assets. Dan could give Sue the right to stay in their family home until she dies but the property would become the property of Dan’s children after Sue passes away. The document safeguards two vital interests because it defends the spouse who survives against losing their home and it ensures the children will receive their inheritance property. The tool functions as an excellent method to solve family disagreements about religious matters in families which include members from different backgrounds.

Mirror Wills (where each spouse’s Will is essentially identical, leaving everything to the other) are common for traditional couples but can be problematic for blended families. If Dan leaves everything to Sue, and Sue later rewrites her Will to leave everything to her biological child, Dan’s children receive nothing. A better approach is for each spouse to have an independent Will that specifically protects their own children’s interests, using life interest provisions, trusts, or direct bequests, rather than relying on the surviving spouse to “do the right thing.” Communication between partners about estate planning is essential, but each person’s Will should independently protect their own family obligations.

Choosing the Right Executor

If any of your children are minors, trusts are especially important in blended family Wills. A trust ensures that your children’s inheritance is managed by a trustee you choose, not by your surviving spouse or their new partner. The trustee can use the funds for your children’s education, healthcare, and living expenses until they reach the age you specify (commonly 18, 19, or 21). Without a trust, a minor’s inheritance could effectively be controlled by the surviving stepparent, which may not reflect your intentions.

The process of choosing an executor becomes vital when you have a blended family structure. Your current spouse will face problems because they must serve as executor while receiving inheritance benefits which could create conflicts between their needs and your children’s needs. The options for naming an executor include choosing an independent third party or a professional executor or appointing co-executors who represent each family branch. The executor should follow your instructions until completion while they protect the rights of your spouse against the needs of children who come from previous relationships.

Dan gives his 16-year-old son $100,000 directly without any trust to hold the funds. The son gains complete access to his funds when he reaches 18 years old after two years have passed. He buys a sports car and spends the rest within a year. The trust would have allowed a trustee to manage the funds for educational expenses and basic needs until the beneficiary reached their 21st or 25th birthday. The trust safeguards both financial resources and child protection against immature financial choices which children make when they are young.

A Power of Attorney for Property designates someone to manage your finances if you become incapacitated. In a blended family, consider whether your current spouse is the best choice or whether an independent person would better protect all parties’ interests. If your spouse manages your finances during incapacity, they could theoretically deplete assets that were intended for your children.

Can Stepchildren Be Included in a Will?

A Living Will records your healthcare wishes, and a healthcare Power of Attorney names who makes medical decisions for you. In blended families, these documents are particularly important because family disagreements about medical care can be amplified when step-relationships are involved. Clear documentation prevents conflict and ensures your wishes are followed. See our guide to advance care terminology for more detail.

Yes. A Will allows you to choose any person you want as a beneficiary including stepchildren and step-grandchildren and other individuals which intestate succession laws do not allow. You have the option to leave them particular presents and define their inheritance percentage and establish them as final recipients of your estate. For blended families, explicitly naming stepchildren is often one of the most important reasons to write a Will. Canadian law prevents stepchildren from receiving any inheritance from their step-parents when these parents pass away because they did not include them in their Wills.

LegalWills.ca offers a LifeLocker feature that allows you to securely store information about your online accounts, passwords, digital assets, and important documents. For blended families, this is especially valuable because it ensures your executor can access everything they need without relying on your surviving spouse’s knowledge or cooperation.

Should Blended Family Spouses Have Mirror Wills?

- Never rely on intestate laws: They do not account for stepchildren or blended family dynamics.

- Consider a life interest: Protects your spouse’s housing while preserving your children’s inheritance.

- Choose executors carefully: Avoid conflicts of interest between spouse and children.

- Use trusts for minors: Keeps your children’s inheritance under independent management.

- Both partners need Wills: Each spouse should have their own Will addressing their specific family obligations.

- Complete your estate plan: Include Powers of Attorney and Living Wills alongside your Will.

- Review and update regularly: Blended family circumstances change. update your Will after any significant family change.

LegalWills.ca makes it straightforward to create a Will that addresses blended family complexities. Start with our step-by-step guide and explore why every Canadian needs a Will.

Tim Hewson is one of the founders of LegalWills.ca.

He has over 20 years of experience helping people to write their Will and other estate planning documents. He has been interviewed by many of the major news media outlets including CTV, Global News, The Toronto Star, and other leading Canadian publications. He has also contributed to a number of financial planning books.

Throughout his career, Tim has written extensively on the subject of Will writing and estate planning.