TL;DR

A trust functions as a legal system which enables trustees to protect and operate assets for the benefit of their designated beneficiaries. People who create their Wills establish testamentary trusts to protect assets which they want to preserve for their minor children and to handle financial matters of beneficiaries who lack financial skills and to care for animals and to handle complicated family dynamics of multiple family units. At LegalWills.ca, you can include trust provisions directly in your Will.

Originally published: June 9, 2022 | Last updated: February 11, 2026

What Is a Trust?

A trust is a legal relationship involving three parties:

- The settlor (or grantor), The person who creates the trust and transfers assets into it

- The trustee, The person or institution responsible for managing the trust assets according to the trust’s terms

- The beneficiary, The person or persons who benefit from the trust assets

Trusts function as essential tools for estate planning because they let you decide when and how people should receive your inherited assets after you pass away. Through a trust you can create specific distribution rules which go beyond giving money directly to your beneficiaries.

For example, rather than leaving $200,000 directly to a 10-year-old child (which is not legally possible in most provinces), you can place that money in a trust managed by a trustee who distributes funds for the child’s education, health, and maintenance until they reach a specified age.

What Is the Difference Between a Living Trust and a Testamentary Trust?

There are two fundamental categories of trusts in Canadian law:

| Feature | Living Trust (Inter Vivos) | Testamentary Trust |

|---|---|---|

| When created | During the settlor’s lifetime | Upon the settlor’s death, through their Will |

| When it takes effect | Immediately upon creation | After probate of the Will |

| Assets transferred | During your lifetime, you must retitle assets | Through your Will after death |

| Probate | Assets in a living trust avoid probate | The Will goes through probate, then the trust is established |

| Tax treatment | Taxed at the highest marginal rate | Graduated tax rates for up to 36 months (qualified disability trusts get graduated rates indefinitely) |

| Cost to set up | $2,000–$10,000+ (requires a lawyer) | Can be included in your Will at minimal additional cost |

| Privacy | Private, not part of public probate records | Will becomes public during probate |

A testamentary trust which you include in your Will stands as the best solution for Canadians because it offers both financial savings and practical benefits. The United States uses living trusts to prevent probate but Canada has low probate fees which make living trusts unnecessary in most provinces except British Columbia and Ontario.

When Should You Include a Trust in Your Will?

There are several common situations where a testamentary trust in your Will is strongly recommended:

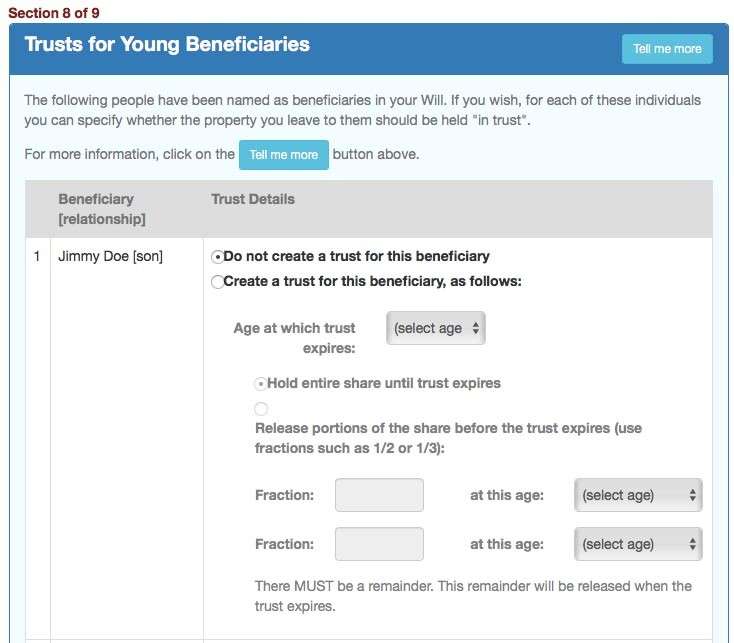

1. Minor Children

Children under 18 cannot legally inherit assets directly in most provinces. The court would select a trustee (Public Guardian and Trustee most of the time) to handle the funds when you leave assets to a child without establishing a trust because you cannot control how the money will be spent. A trust in your Will lets you:

- Name a specific trustee you trust

- Specify how funds should be used (education, health, maintenance)

- Set the age at which the child receives the remaining funds (e.g., 25 instead of 18)

- Provide for staggered distributions (e.g., one-third at 21, one-third at 25, remainder at 30)

For more on protecting your children in your Will, see our guide on what to include in a Will if you have children.

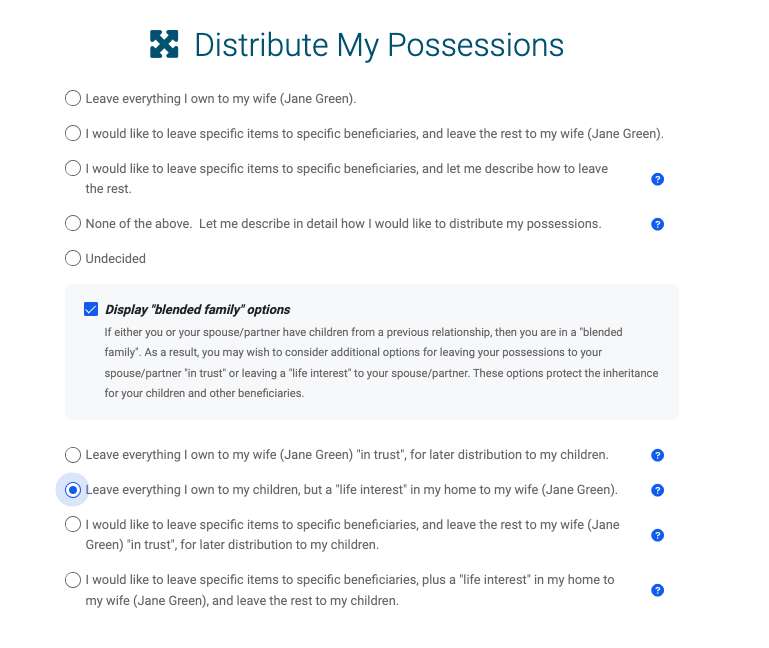

2. Blended Families

Trusts serve as effective tools to solve conflicting interests which people face when they enter their second marriage or when they have children from different relationships. A spousal life interest trust operates as a common method which allows your surviving spouse to live in the family home while receiving income from your estate until death but protects the capital value for your children from previous relationships.

Without a trust, there is a real risk that assets intended for your children could pass entirely to your surviving spouse’s family. Our article on Wills for blended families explains these concepts in greater detail.

3. Beneficiaries with Disabilities

A Henson trust (also called an absolute discretionary trust) is specifically designed for beneficiaries who receive provincial disability benefits. If you leave assets directly to a person with a disability, they may lose their government benefits. A Henson trust gives the trustee absolute discretion over distributions, meaning the trust assets are not counted as the beneficiary’s personal assets for benefit eligibility purposes.

4. Beneficiaries Who Cannot Manage Finances

A spendthrift trust protects assets and beneficiaries when a beneficiary needs financial protection because they have shown poor money management skills or addiction problems or they cannot handle receiving a large inheritance all at once.

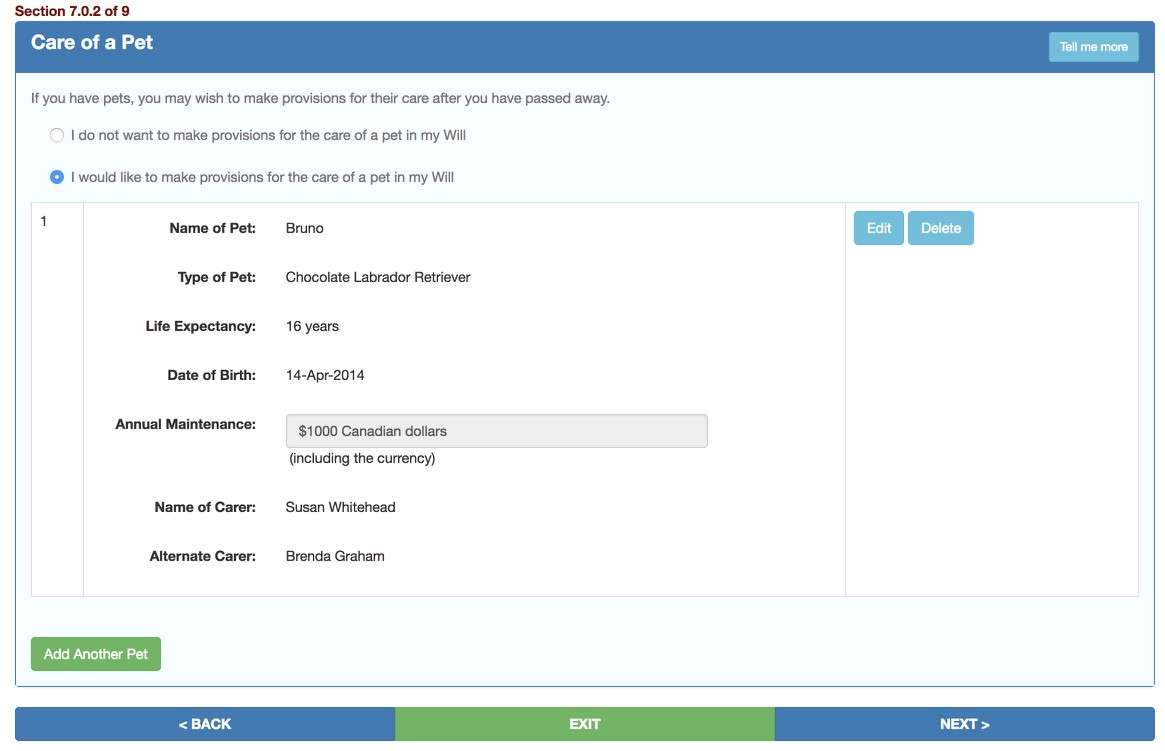

5. Pet Trusts

Canadian law allows you to create a trust for the care of your pets. A pet trust names a caregiver and sets aside funds for your pet’s food, veterinary care, and other needs. The trustee manages the funds and ensures they are used for the pet’s benefit.

For a detailed guide on setting up a pet trust, see our article on setting up a pet trust.

How Do You Set Up a Trust in Your Will?

You need to add particular trust provisions to your Will when you want to establish a testamentary trust. The key elements you need to define are:

- The trustee. Choose a reliable, financially responsible person or institution. The trustee must handle trust assets through fiduciary responsibilities which protect beneficiary interests during all management activities. You should select a backup trustee because your main choice might become unavailable for their duties.

- The beneficiary or beneficiaries, Clearly identify who benefits from the trust.

- The trust assets, Specify which assets go into the trust. This can be specific assets (e.g., the family home) or a portion of your residual estate.

- Distribution terms. Define when and how the trustee should distribute assets. This includes:

What expenses the trustee can pay from the trust (education, health, maintenance)

Whether the trustee can distribute capital or only income

At what age or milestone the trust terminates and remaining assets are distributed - Trustee powers, Specify what investment and management powers the trustee has.

- Trustee compensation, Whether and how the trustee will be compensated for their work. See our article on Executor and trustee fees.

Through LegalWills.ca you can create trust provisions for minor children which become part of your Will by using their online guided service. For complicated trust arrangements you need to seek help from an estate planning lawyer.

What Are the Tax Implications of Trusts in Canada?

The Canadian trust taxation system experienced a major overhaul because of the 2016 federal budget which introduced new rules. Key points:

- Testamentary trusts created after December 31, 2015 are taxed at the highest marginal tax rate on any retained income, except for the first 36 months after death (the “graduated rate estate” period) when graduated rates apply.

- The graduated tax rates continue to apply indefinitely to qualified disability trusts which serve beneficiaries who qualify for the Disability Tax Credit.

- Living trusts have always been taxed at the highest marginal rate.

- The 21-year deemed disposition rule requires trusts to pay capital gains tax every 21 years as if trust assets were sold at fair market value, even if no actual sale occurs.

These tax rules mean that trusts should be used for genuine estate planning purposes, not primarily as tax avoidance vehicles. A tax professional needs to provide you with specific guidance based on your individual circumstances.

Common Mistakes When Creating Trusts

Avoid these common errors when including trust provisions in your Will:

- Choosing the wrong trustee, A trustee must be trustworthy, financially competent, and willing to serve for potentially many years. Avoid selecting any person who maintains a relationship that could cause a conflict when dealing with the beneficiary.

- Vague distribution terms. Terms like “as needed” or “for their benefit” are too vague. Be specific: “for education expenses, medical costs, and reasonable living expenses.”

- No alternate trustee, If your chosen trustee dies, becomes incapacitated, or refuses to act, the court will appoint a replacement. Name an alternate to maintain control.

- Underfunding the trust. Ensure enough assets are allocated to the trust to achieve its purpose. A trust for a minor child’s care until age 25 needs enough capital to sustain 7+ years of expenses.

- Ignoring trustee compensation. Managing a trust is significant work. If you do not address compensation, provincial trustee compensation rules apply, which may not match your intentions.

- Not updating the trust provisions, As circumstances change, your trust provisions should be reviewed and updated accordingly.

Frequently Asked Questions

Do I need a lawyer to set up a trust?

Not necessarily. Simple testamentary trusts for minor children can be included in your Will through an online service like LegalWills.ca. For complex trust arrangements, such as Henson trusts for disabled beneficiaries, spousal trusts, or trusts involving business assets, consulting an estate planning lawyer is recommended.

Can a trustee also be a beneficiary?

The answer is yes but this arrangement creates a potential conflict when trying to resolve different interests. The trustee needs to appoint a co-trustee or independent advisor who will handle all distribution decisions when the trustee also serves as a beneficiary.

How long can a trust last?

In most Canadian provinces, a trust can last for up to 21 years after the death of the last named beneficiary who was alive when the trust was created (the rule against perpetuities). The rule no longer applies in Manitoba and some trust types in various jurisdictions after these provinces decided to change or eliminate this regulation. The 21-year deemed disposition tax rule applies regardless.

Can I create a trust without a Will?

Yes. A living trust (inter vivos trust) is created during your lifetime through a separate trust deed, independent of your Will. A lawyer needs to create your living trust because this process requires you to transfer your assets during life which leads to immediate tax consequences.

What happens to a trust if the trustee dies?

If you named an alternate trustee in your Will, that person takes over. If no alternate was named, the court will appoint a replacement trustee. This is why naming an alternate trustee is essential.

Tim Hewson is one of the founders of LegalWills.ca.

He has over 20 years of experience helping people to write their Will and other estate planning documents. He has been interviewed by many of the major news media outlets including CTV, Global News, The Toronto Star, and other leading Canadian publications. He has also contributed to a number of financial planning books.

Throughout his career, Tim has written extensively on the subject of Will writing and estate planning.