Originally published: May 27, 2016 | Last updated: January 8, 2025

TL;DR: Digital assets – social media accounts, email, cloud storage, online banking, cryptocurrency, and digital subscriptions – are an increasingly important part of estate planning. Without a plan, your executor may be unable to access, manage, or close your online accounts. LegalWills.ca offers a LifeLocker feature to securely catalogue your digital assets and a Keyholders system to ensure your executor can access them.

Digital assets include all online accounts together with digital files and electronic property which hold financial value and sentimental worth and practical usefulness. People across Canada now maintain multiple digital accounts which have grown into essential digital property values that keep rising each year. The digital assets need classification into three primary groups which include:

Digital assets are any online accounts, digital files, or electronic property that have value; financial, sentimental, or practical. The average Canadian has dozens of digital accounts, and these assets are growing in number and importance every year. Digital assets fall into three main categories:

Social Assets

Social media accounts (Facebook, Instagram, X/Twitter, LinkedIn), messaging apps, forums, and online communities. These accounts contain your personal history, photos, connections, and communications. After death, some platforms offer memorialization options, but your executor needs access to manage or close these accounts according to your wishes.

Social media accounts (Facebook, Instagram, X/Twitter, LinkedIn), messaging apps, forums, and online communities. The accounts store your personal records which include photos together with your communication history and contact list. After death, some platforms offer memorialization options, but your executor needs access to manage or close these accounts according to your wishes.

Cloud-stored photos (Google Photos, iCloud), email archives (Gmail, Outlook), digital music and video libraries, blogs, personal websites, and documents stored in cloud services (Dropbox, Google Drive, OneDrive). These may have no financial value but are irreplaceable personal records that families may want to preserve or that your executor needs to access during estate administration.

Sentimental Assets

Online banking, investment platforms, PayPal and other payment services, cryptocurrency wallets, domain names, revenue-generating websites, e-commerce stores, digital intellectual property, and online subscriptions with recurring charges. These assets have direct financial value and must be identified, managed, and either transferred or closed by your executor. Cryptocurrency is particularly challenging, without private keys or wallet access, crypto assets can be permanently lost.

Cloud-stored photos (Google Photos, iCloud), email archives (Gmail, Outlook), digital music and video libraries, blogs, personal websites, and documents stored in cloud services (Dropbox, Google Drive, OneDrive). The documents lack monetary worth but they represent personal family records which require protection during estate distribution and should stay accessible to your executor.

Traditional estate planning focuses on physical property and financial accounts held at known institutions. Digital assets create unique challenges:

- Access barriers: Online accounts are protected by passwords, two-factor authentication, and encryption. Without credentials, your executor cannot access them.

- Terms of service: Many platforms prohibit sharing login credentials and have their own policies for deceased users’ accounts, which may conflict with your wishes.

- Invisibility: Unlike a bank statement or property deed, digital assets leave no physical trail. Your executor may not even know they exist.

- Recurring costs: Subscriptions, domain renewals, hosting fees, and storage plans continue charging after death unless someone cancels them.

- Security risk: Unmanaged accounts can be hacked, leading to identity theft using the deceased person’s information.

Financial Assets

Some people name a separate “digital executor”, someone specifically tasked with managing their online accounts after death. This person is typically more tech-savvy than a traditional executor and understands how to navigate different platforms’ policies for deceased users. While Canadian law does not formally recognize a separate “digital executor” role, you can include instructions in your Will designating someone to handle your digital assets, or you can provide specific guidance to your main executor about your digital wishes.

The banking system operates through online platforms which allow users to access their accounts and perform transactions while PayPal and other payment services and cryptocurrency wallets and domain names and revenue websites and e-commerce stores and digital intellectual property and online subscriptions with recurring charges serve as financial assets. The executor needs to identify these assets which possess direct financial worth so they can handle their transfer or closure process. The loss of crypto assets becomes permanent because users cannot retrieve private keys or access their cryptocurrency wallets.

LegalWills.ca provides two tools specifically designed for digital asset planning:

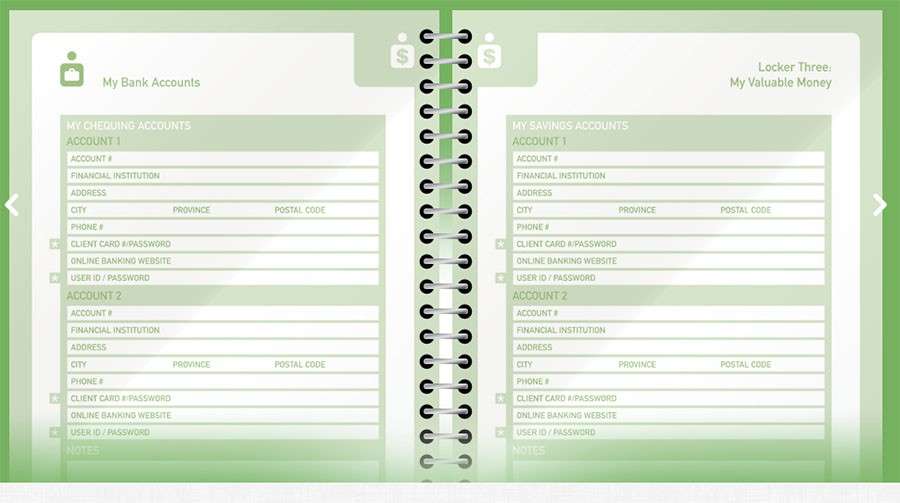

LifeLocker: A secure digital vault where you can catalogue all your online accounts, passwords, security questions, cryptocurrency wallet information, and any other digital asset details. This information is encrypted and stored securely, accessible only to the people you designate.

Keyholders: A notification system that alerts designated trusted individuals about the existence and location of your LifeLocker information and your Will. This ensures that the right people can access your digital assets when the time comes, without having to search for scattered passwords and account information.

Start your digital estate plan alongside your Last Will and Testament. For broader estate planning context, see our definitions guide and learn why every Canadian needs a Will.

Tim Hewson is one of the founders of LegalWills.ca.

He has over 20 years of experience helping people to write their Will and other estate planning documents. He has been interviewed by many of the major news media outlets including CTV, Global News, The Toronto Star, and other leading Canadian publications. He has also contributed to a number of financial planning books.

Throughout his career, Tim has written extensively on the subject of Will writing and estate planning.